This week, we have chosen to focus on Excelsior Mining, an example of how old technologies with new applications can be troublesome, how the devil is in the detail, and how not doing enough preparatory work creates major problems for mining companies.

Overview

Excelsior Mining ("Excelsior) (OTCQX:EXMGF) (TSX:MIN) (FSE: 3X3) has a market capitalisation of ~C$260 million, it has just started production from its in-situ leach Gunnison copper project, and is marketing itself with the catchy slogan “We make copper green”.

Not only that, but the share price has almost doubled in recent months on the back of the promise that production would start in 2020, and the Gunnison is in the pro-mining, copper-rich, low-risk state of Arizona. So much to like!

Interestingly the “Excelsior Mining Produces First Copper Cathode” news on 21 December was just a very brief statement, making it seem as if the Company had technically kept its promise, but it did not have a lot of detail to shout about. When we, the good folk at Crux Investor, see something like that, it makes us curious. Is there more to the story? What is really going on?

What follows is a seriously technical analysis of the project, and how the Company has addressed the implementation of the pioneering extraction method on this particular geology. Not wanting to beat around the bush, we can tell you that the company has had to make so many major adaptations that the key de-risking document, the feasibility study, is now largely irrelevant. All inputs and expectations are up in the air.

Indeed there are many risks and pitfalls for the Company that we explain below. All of these factors are likely to have a major effect on contained metal in reserves, metallurgical recovery, acid consumption, operating cost and sustaining capital expenditure. While we love the idea of producing low-carbon, green copper in Arizona, sadly it is largely irrelevant unless the company can prove sustainable and commercial production at an economic cost.

The Gunnison project again proves the risks of being a pioneer in adopting new technologies. When the go-ahead for any new project, let alone one that incorporates a new technology, is given without substantial empirical evidence and pilot plant work, investors should realise they taken on extremely high risk. We feel that Excelsior Mining is now, and will remain for the foreseeable future, a long way from sustainable and commercial production.

.png)

For those who do not want to read all the detail further below, this report shows that there are a number of conceptual risks with the business model in terms of geology, geohydrological and metallurgical assumptions, which seem to be borne out by the actual early production, requiring the company to substantially move away from the feasibility study plan. The fact that first copper cathode production was achieved is of little relevance until sustained commercial production is achieved. Caveat Emptor (let the buyer beware)…

What the Company reports

Excelsior has been involved with the Gunnison project in Arizona, USA, since 2007. Along the way it has completed a Feasibility Study (2014, updated in 2016), and bought a defunct heap leach operation called Johnson Camp mine (“JCM”) complete with a solvent extraction electrowinning (“SX-EW”) plant with a capacity to produce 25 million pounds (“Mlb”) per annum.

The feasibility study envisaged production of copper by means of in-situ leaching of a large, low-grade copper deposit and included a three-stage production ramp up, the first using the JCM plant. The economics of the project were (according to the feasibility study) amazingly attractive with an NPV7.5 of US$807M for initial investment of less than US$47M. The study envisaged a nine months “construction” period, which essentially would comprise drilling of injection and extraction boreholes and piping to the plant.

The idea of in-situ leaching is very attractive to bankers and investors as it offers the prospect of not having to go through the dirty business of actually mining rock. Capital expenditure is low, earth disturbance is minimal, and everyone is happy and makes money. Right? Well, not always…

What the Analysts see

Leaching of copper minerals using acid is a proven processing method used in heap leach operations globally. Applying the leaching of copper minerals to in-situ leaching, however, is very unusual. And it is unusual because for it to work, an unusual set of preconditions are needed:

- Copper must be present in minerals amenable to acid leaching.

- No other minerals that consume acid should be present in meaningful quantities, otherwise acid consumption (and overall acid cost) will be prohibitive.

- The deposit must be below the water table, otherwise the injected solution will drain down to the water table.

- The copper mineralisation must occur in permeable rocks with manageable fracturing and flow dynamics so that the leaching fluids can access the copper across a sufficient rock mass.

- The deposit would ideally be encased in impermeable rocks to minimise leakage of acid or pregnant solution away from the deposit.

Excelsior management states quite accurately in their corporate presentation that the method is a very established mining method for Uranium, but this is slightly disingenuous. Although acid is the main leaching agent in Kazakhstan, in the USA the use of an alkali leach is preferred due to the presence of significant quantities of acid-consuming minerals such as gypsum and limestone in the host aquifers.

And this is where the geology comes into play. The Excelsior leaching operation is in an area described as a classic skarn type deposit in contact with an intrusion. Skarns form through metamorphic processes as igneous intrusions react with host rock. The intrusions often interact with limestones, where metals and hot fluids mix, new minerals are formed and then everything cools down as a skarn. After formation, later erosion can expose skarns to the surface where weathering and oxidation of sulphide minerals take place.

Remember that fluid flows preferentially along fractures, and through permeable lithologies. Skarns form preferentially when acidic fluids meet with reactive lithologies (such as limestone). At Gunnison primary mineralisation is related to three main factors:

- Proximity to the intrusion

- Fracture intensity

- Lithology (permeability and reactiveness)

Overprinting that all is an oxidation profile which is the most recent event affecting the sulphides.

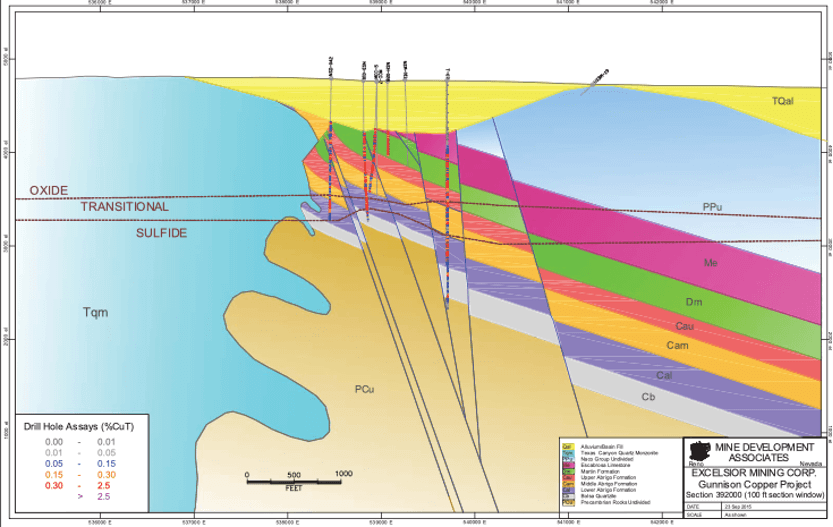

At Gunnison, the sulphides at the upper levels of North Star have been oxidised by meteoric water, with copper now mostly present in chrysocolla (Cu₂H₂Si₂O₅(OH)₄) as fracture fillings and vein fill. Chrysocolla is soluble in sulphuric acid, although it is not strictly an oxide mineral. For the geologically-minded among you, it’s hydrated copper phyllosilicate. (Ed….Taxi!)

The cross section also shows the vertical depth of the boundaries to Transitional and Sulfide mineralisation where the copper ceases to be leachable. The criterion used for Oxide mineralisation is a soluble copper grade (“CuAs”) constituting more than half the total copper grade (“CuT”).

As noted above, the development of primary copper-sulphide skarn mineralisation is related to the proximity to the intrusion. The skarn mineralisation preferentially developed in carbonate-bearing units, with the combination of this and proximity to the intrusion leading to the Martin (green colour) and Abrigo Formations (red, yellow and violet) being the primary host units.

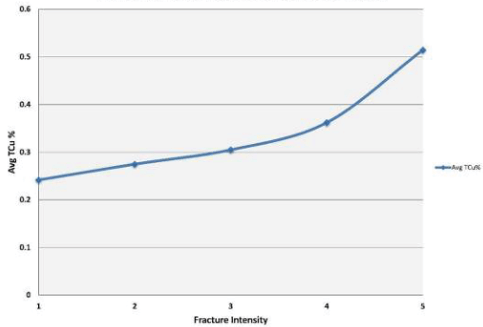

According to the feasibility study report there is a strong correlation between total Cu-grade and fracture intensity varying from 0.23% Cu for low intensity fracturing Intensity 1 (defined as less than 5% of core length with pieces less than 10 cm long) to 0.53% Cu for an Intensity 5 (defined as 80%-100% of the drill core pieces being less than 10 cm long) (see Figure 3). This is intuitive because in a skarn, mineralisation is related to fluid flow, and were there are more fractures, there is more copper.

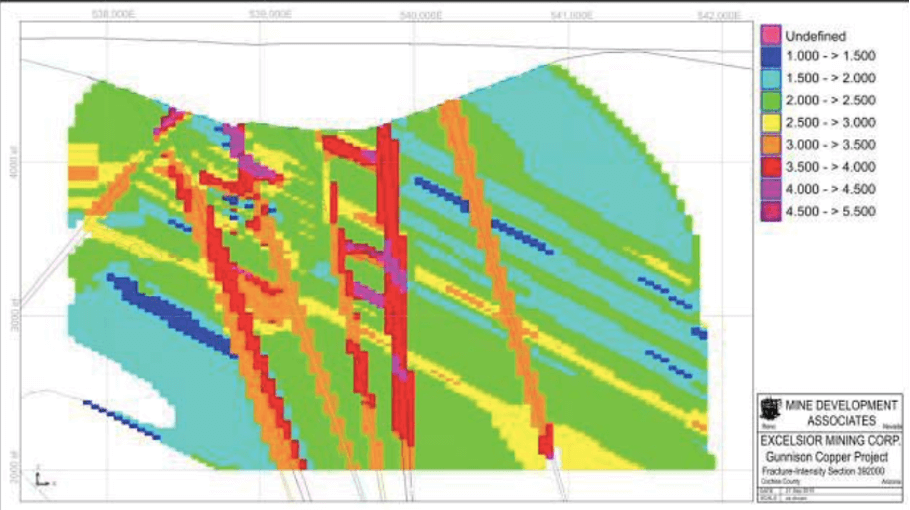

To really dig into the detail, fracture intensity is controlled by several factors: fracturing related to volume loss during skarn development, and fracturing related to pre- and post-mineral faulting. Figure 4 shows the modelled fracture intensity from borehole logs illustrating the strong association with relatively steep faults and a weaker (and thinner) trend parallel to bedding.

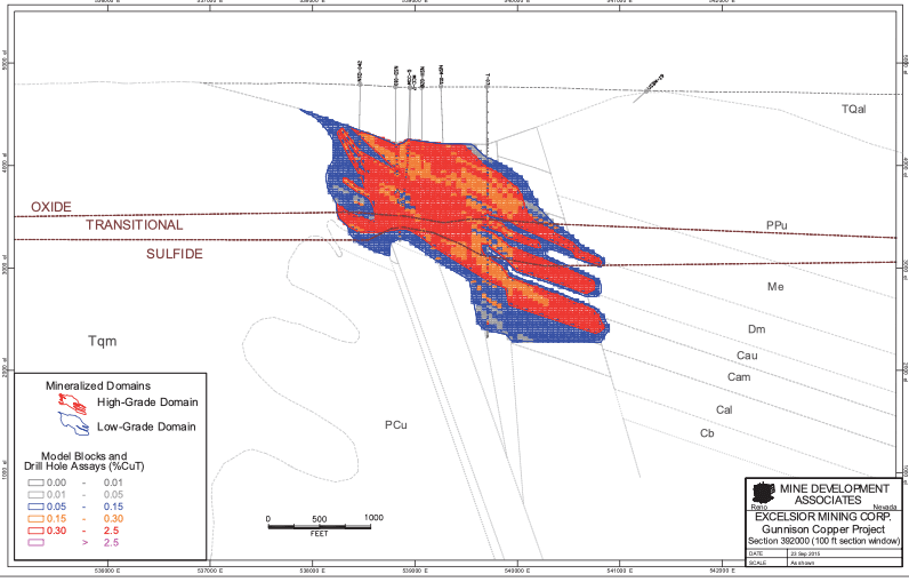

The above relationship is however not evident in the block model for North Star as is shown in Figure 5, which is along the same cross section as in Figure 4 implying that the faults are dominantly post mineralisation.

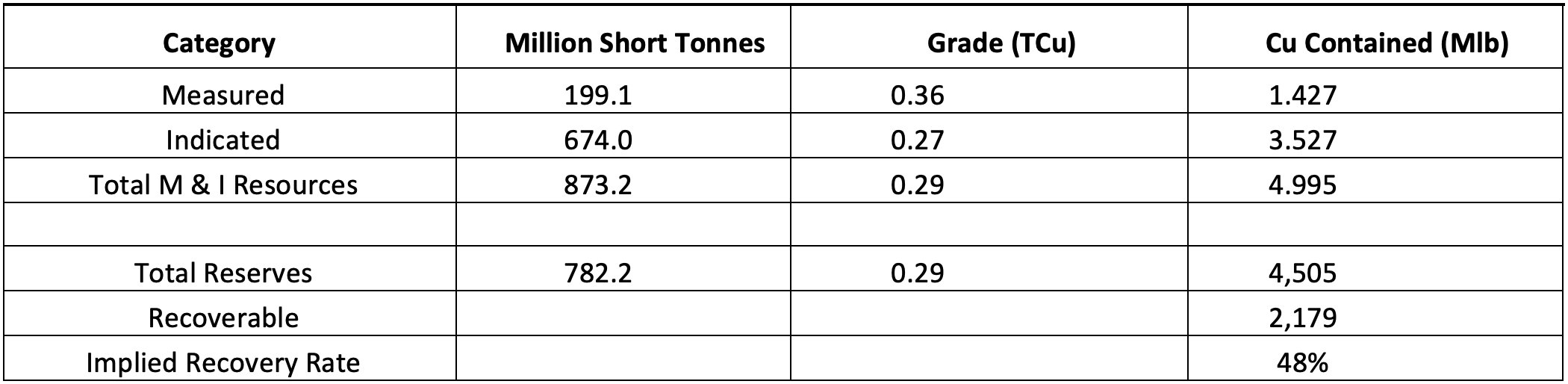

Table 1 shows the mineral resources at a 0.05% TCu cut-off grade and mineral reserves estimated for North Star.

The reserves are essentially the same as resources, but dropping out mineralisation below the Interstate 10 road.

Original Business Plan

Leaching was envisaged by each “production cell” having a central injection well surrounded by four recovery wells on the corners of the square defined by this pattern and each at 30 m distance of the injection cell.

What is a sweep factor, and why should you care?

According to the feasibility study, the amount of recoverable copper depends on something called a Sweep Factor, specific gravity (defined as % of available copper that is contacted by leach solution) and acid soluble copper grade for that 30 m x 30 m x 8 m block of the resource block model.

The sweep factor represents the calculated recovery based on the fracture intensity assigned to the resource block model with an assumed relationship of 20% for Fracture Intensity 1 to more than 80% for Fracture Intensity 3 (20%-50% of the core pieces below 10 cm long) and above. Or in simpler words, the Sweep Factor is a way for Excelsior Mining to make an in-situ recovery estimate from any given block, based on a combination of grade and fracture intensity.

The forecast metallurgical recovery is based on laboratory tests combined with simulation models, not on empirically established factors through a pilot scheme. Therefore, the claim by Excelsior that the injection solution recovery (“ISR”) metallurgical parameters have been established at a feasibility level of confidence sits awkwardly with six assumptions in the section on mineral processing and the 16 mentions of “estimates” or “estimating” in that section of the technical report.

The business plan assumed a stage increase in production, initially at a rate of less than 1,000 t Cu per month, doubling this for Stage 2 in production year 3 and doubling this again for Stage 3 in production years 5 and 6.

What it means for Investors

Potential investors should note that some large players (Magma Copper, BHP and Phelps Dodge) investigated and then rejected further work on this project. Magma Copper actually got to the point of carrying out test work before choosing not to continue. No details of this historic work are provided by Excelsior.

The business plan is based on modelling with major assumptions on how the injected fluid behaves and on achievable leach recovery and on acid consumption. Of particular concern to us, with respect to assumptions, are:

- The assumed Sweep Factor of 80% for rock with a Fracture Intensity with 20%-50% core pieces of less than 10 cm seems overly optimistic.

- The behaviour of solution movement is unlikely to be uniform and unaffected by differences in permeability. In practice fluid movement will prefer the pathways of least resistance, so-called channelling. The geological model and cross section for Fracture Intensity clearly point to the risk of channelling, both along bedding and especially along steeper fault structures. Channelling would greatly reduce the sweep factor by sterilising large volumes of low Fracture Intensity mineralisation from being exposed to the acid solution.

- Whereas there is mention of clay minerals close to the intrusive/skarn contact, exactly where the highest-grade copper mineralisation is present, their effect on permeability seems to be ignored.

- The amount of acid consumed seems to totally ignore the possibility of carbonate minerals and iron oxides affecting the total required. Acid consumption of 10 lb of acid per lb of recovered Cu is very low compared to conventional (non-in-situ) copper leaching operations.

- The economic valuation seems to ignore the cost of drilling the overburden.

- The reference by Excelsior to Taseko’s nearby Florence ISR operation, where a pilot programme proved to be successful, is misleading. The Florence deposit is a copper porphyry that was uplifted to surface and subjected to weathering and oxidation processes before being covered by younger lithologies. The hydraulic conditions have been proven suitable by extensive historical testwork.

Not wanting to be a complete killjoy, there is also an opportunity for Excelsior.

Whereas channelling is a major risk to recover copper from the total skarn package, it creates an opportunity to focus drilling and extraction of the copper along high permeability structures. The geological information points to these structures having the highest grade and (probably) highest CuAS/TCu ratios. The implication is that the kinetics and speed of fluid flow will be such that copper recovery will be fast, requiring less infrastructure and plant.

It would require detailed definition of such targets and accurately intersecting these by drilling of injection and extraction wells. A consequence of this approach is that the channels are a small fraction of the overall volume of the mineralised rock mass, and high-grading would affect the rest of the resource.

Developments since go-ahead decision

After start of construction in December 2018 it took a full year to complete the Stage 1 project which comprised 41 injection and recovery wells and 16 compliance and monitoring wells all to depths of approx. 400m depth. Total project capital expenditure at this stage was US$76M (remember the US$47M per feasibility study?).

Injection of mining fluids started on 31 December 2019 covering an area of 120m x 120 m x 210m (depth) in a closed loop system until the copper in solution reached the required threshold for treatment in the SX-EW plant. Whereas the company claimed that in January 2020 performance levels exceeded feasibility study levels, this was clearly not the full story as in February 2020 it announced it had

“initiated several optimizimation changes to the production wellfield”. The measures were to “assist in acid breakthrough and continued copper mobilization. Breakthrough will be achieved when free acid is detected at designated recovery wells; thereby maintaining the desired pH level (acidity level) where copper will remain in solution”.

Specifically, the wells were made amenable to reverse the fluid flow. In other words, a particular well would be able to first inject and then extract the fluid. The company also announced:

“In parallel, infrastructure is being installed that will allow for concentrated acid to be injected into each well, which will dissolve any reprecipitated copper (copper sulphate) in the area of the pumps, thereby ensuring effective fluid flow. Preventative maintenance programs to limit pump and wellfield down-time are also being implemented”.

The above problems point to:

- The injected fluid not being able to reach the extraction wells.

- Acid being consumed, with the resulting drop in pH resulting in dissolved copper again precipitating.

- Problems with keeping the wells operating properly.

In April 2020 the company used the COVID-19 pandemic as a useful excuse to place the project on care-and-maintenance, to restart an a “small scale” in August. By 30 September 2020 the company had spent another US$6.7M on the project.

With injecting concentrated sulphuric acid solution the problem of precipitated copper was solved (no mention of what the effect was on acid consumption) and the extraction of copper could begin in December leading to the first cathode production. In parallel “expansion of activities to surrounding wells is occurring, with a view to ramping-up to full, nameplate, capacity through 2021”.

Conclusion

The company has had to overhaul the way in which it leaches copper making the feasibility study less of a final and definitive document than the Company would have hoped. Inputs and expectations of production, resource base, and costs are up in the air. It seems that the concerns expressed previously may well be applicable which would have a detrimental effect on contained metal in reserves, metallurgical recovery, acid consumption, operating cost and sustaining capital expenditure.

The fact that copper has been produced is encouraging but more of a marketing ploy than an indication of technical success. It will be important for the company to demonstrate sustainable commercial production at acceptable costs. The Gunnison project again proves the risks of being a pioneer in adopting new technologies. When the go-ahead for any new project, let alone one that incorporates a new technology, is given without substantial empirical evidence and pilot plant work, investors should realise they taken on extremely high risk. Caveat Emptor.

If you are a Family Office investor, or an Institutional investor, and you would like the full report behind this article, please contact matthew@cruxinvestor.com

This week, we have chosen to focus on Excelsior Mining, an example of how old technologies with new applications can be troublesome, how the devil is in the detail, and how not doing enough preparatory work creates major problems for mining companies.

Overview

Excelsior Mining ("Excelsior) (OTCQX:EXMGF) (TSX:MIN) (FSE: 3X3) has a market capitalisation of ~C$260 million, it has just started production from its in-situ leach Gunnison copper project, and is marketing itself with the catchy slogan “We make copper green”.

Not only that, but the share price has almost doubled in recent months on the back of the promise that production would start in 2020, and the Gunnison is in the pro-mining, copper-rich, low-risk state of Arizona. So much to like!

Interestingly the “Excelsior Mining Produces First Copper Cathode” news on 21 December was just a very brief statement, making it seem as if the Company had technically kept its promise, but it did not have a lot of detail to shout about. When we, the good folk at Crux Investor, see something like that, it makes us curious. Is there more to the story? What is really going on?

What follows is a seriously technical analysis of the project, and how the Company has addressed the implementation of the pioneering extraction method on this particular geology. Not wanting to beat around the bush, we can tell you that the company has had to make so many major adaptations that the key de-risking document, the feasibility study, is now largely irrelevant. All inputs and expectations are up in the air.

Indeed there are many risks and pitfalls for the Company that we explain below. All of these factors are likely to have a major effect on contained metal in reserves, metallurgical recovery, acid consumption, operating cost and sustaining capital expenditure. While we love the idea of producing low-carbon, green copper in Arizona, sadly it is largely irrelevant unless the company can prove sustainable and commercial production at an economic cost.

The Gunnison project again proves the risks of being a pioneer in adopting new technologies. When the go-ahead for any new project, let alone one that incorporates a new technology, is given without substantial empirical evidence and pilot plant work, investors should realise they taken on extremely high risk. We feel that Excelsior Mining is now, and will remain for the foreseeable future, a long way from sustainable and commercial production.

For those who do not want to read all the detail further below, this report shows that there are a number of conceptual risks with the business model in terms of geology, geohydrological and metallurgical assumptions, which seem to be borne out by the actual early production, requiring the company to substantially move away from the feasibility study plan. The fact that first copper cathode production was achieved is of little relevance until sustained commercial production is achieved. Caveat Emptor (let the buyer beware)…

What the Company reports

Excelsior has been involved with the Gunnison project in Arizona, USA, since 2007. Along the way it has completed a Feasibility Study (2014, updated in 2016), and bought a defunct heap leach operation called Johnson Camp mine (“JCM”) complete with a solvent extraction electrowinning (“SX-EW”) plant with a capacity to produce 25 million pounds (“Mlb”) per annum.

The feasibility study envisaged production of copper by means of in-situ leaching of a large, low-grade copper deposit and included a three-stage production ramp up, the first using the JCM plant. The economics of the project were (according to the feasibility study) amazingly attractive with an NPV7.5 of US$807M for initial investment of less than US$47M. The study envisaged a nine months “construction” period, which essentially would comprise drilling of injection and extraction boreholes and piping to the plant.

The idea of in-situ leaching is very attractive to bankers and investors as it offers the prospect of not having to go through the dirty business of actually mining rock. Capital expenditure is low, earth disturbance is minimal, and everyone is happy and makes money. Right? Well, not always…

What the Analysts see

Leaching of copper minerals using acid is a proven processing method used in heap leach operations globally. Applying the leaching of copper minerals to in-situ leaching, however, is very unusual. And it is unusual because for it to work, an unusual set of preconditions are needed:

- Copper must be present in minerals amenable to acid leaching.

- No other minerals that consume acid should be present in meaningful quantities, otherwise acid consumption (and overall acid cost) will be prohibitive.

- The deposit must be below the water table, otherwise the injected solution will drain down to the water table.

- The copper mineralisation must occur in permeable rocks with manageable fracturing and flow dynamics so that the leaching fluids can access the copper across a sufficient rock mass.

- The deposit would ideally be encased in impermeable rocks to minimise leakage of acid or pregnant solution away from the deposit.

Excelsior management states quite accurately in their corporate presentation that the method is a very established mining method for Uranium, but this is slightly disingenuous. Although acid is the main leaching agent in Kazakhstan, in the USA the use of an alkali leach is preferred due to the presence of significant quantities of acid-consuming minerals such as gypsum and limestone in the host aquifers.

And this is where the geology comes into play. The Excelsior leaching operation is in an area described as a classic skarn type deposit in contact with an intrusion. Skarns form through metamorphic processes as igneous intrusions react with host rock. The intrusions often interact with limestones, where metals and hot fluids mix, new minerals are formed and then everything cools down as a skarn. After formation, later erosion can expose skarns to the surface where weathering and oxidation of sulphide minerals take place.

Remember that fluid flows preferentially along fractures, and through permeable lithologies. Skarns form preferentially when acidic fluids meet with reactive lithologies (such as limestone). At Gunnison primary mineralisation is related to three main factors:

- Proximity to the intrusion

- Fracture intensity

- Lithology (permeability and reactiveness)

Overprinting that all is an oxidation profile which is the most recent event affecting the sulphides.

At Gunnison, the sulphides at the upper levels of North Star have been oxidised by meteoric water, with copper now mostly present in chrysocolla (Cu₂H₂Si₂O₅(OH)₄) as fracture fillings and vein fill. Chrysocolla is soluble in sulphuric acid, although it is not strictly an oxide mineral. For the geologically-minded among you, it’s hydrated copper phyllosilicate. (Ed….Taxi!)

The cross section also shows the vertical depth of the boundaries to Transitional and Sulfide mineralisation where the copper ceases to be leachable. The criterion used for Oxide mineralisation is a soluble copper grade (“CuAs”) constituting more than half the total copper grade (“CuT”).

As noted above, the development of primary copper-sulphide skarn mineralisation is related to the proximity to the intrusion. The skarn mineralisation preferentially developed in carbonate-bearing units, with the combination of this and proximity to the intrusion leading to the Martin (green colour) and Abrigo Formations (red, yellow and violet) being the primary host units.

According to the feasibility study report there is a strong correlation between total Cu-grade and fracture intensity varying from 0.23% Cu for low intensity fracturing Intensity 1 (defined as less than 5% of core length with pieces less than 10 cm long) to 0.53% Cu for an Intensity 5 (defined as 80%-100% of the drill core pieces being less than 10 cm long) (see Figure 3). This is intuitive because in a skarn, mineralisation is related to fluid flow, and were there are more fractures, there is more copper.

To really dig into the detail, fracture intensity is controlled by several factors: fracturing related to volume loss during skarn development, and fracturing related to pre- and post-mineral faulting. Figure 4 shows the modelled fracture intensity from borehole logs illustrating the strong association with relatively steep faults and a weaker (and thinner) trend parallel to bedding.

The above relationship is however not evident in the block model for North Star as is shown in Figure 5, which is along the same cross section as in Figure 4 implying that the faults are dominantly post mineralisation.

Table 1 shows the mineral resources at a 0.05% TCu cut-off grade and mineral reserves estimated for North Star.

The reserves are essentially the same as resources, but dropping out mineralisation below the Interstate 10 road.

Original Business Plan

Leaching was envisaged by each “production cell” having a central injection well surrounded by four recovery wells on the corners of the square defined by this pattern and each at 30 m distance of the injection cell.

What is a sweep factor, and why should you care?

According to the feasibility study, the amount of recoverable copper depends on something called a Sweep Factor, specific gravity (defined as % of available copper that is contacted by leach solution) and acid soluble copper grade for that 30 m x 30 m x 8 m block of the resource block model.

The sweep factor represents the calculated recovery based on the fracture intensity assigned to the resource block model with an assumed relationship of 20% for Fracture Intensity 1 to more than 80% for Fracture Intensity 3 (20%-50% of the core pieces below 10 cm long) and above. Or in simpler words, the Sweep Factor is a way for Excelsior Mining to make an in-situ recovery estimate from any given block, based on a combination of grade and fracture intensity.

The forecast metallurgical recovery is based on laboratory tests combined with simulation models, not on empirically established factors through a pilot scheme. Therefore, the claim by Excelsior that the injection solution recovery (“ISR”) metallurgical parameters have been established at a feasibility level of confidence sits awkwardly with six assumptions in the section on mineral processing and the 16 mentions of “estimates” or “estimating” in that section of the technical report.

The business plan assumed a stage increase in production, initially at a rate of less than 1,000 t Cu per month, doubling this for Stage 2 in production year 3 and doubling this again for Stage 3 in production years 5 and 6.

What it means for Investors

Potential investors should note that some large players (Magma Copper, BHP and Phelps Dodge) investigated and then rejected further work on this project. Magma Copper actually got to the point of carrying out test work before choosing not to continue. No details of this historic work are provided by Excelsior.

The business plan is based on modelling with major assumptions on how the injected fluid behaves and on achievable leach recovery and on acid consumption. Of particular concern to us, with respect to assumptions, are:

- The assumed Sweep Factor of 80% for rock with a Fracture Intensity with 20%-50% core pieces of less than 10 cm seems overly optimistic.

- The behaviour of solution movement is unlikely to be uniform and unaffected by differences in permeability. In practice fluid movement will prefer the pathways of least resistance, so-called channelling. The geological model and cross section for Fracture Intensity clearly point to the risk of channelling, both along bedding and especially along steeper fault structures. Channelling would greatly reduce the sweep factor by sterilising large volumes of low Fracture Intensity mineralisation from being exposed to the acid solution.

- Whereas there is mention of clay minerals close to the intrusive/skarn contact, exactly where the highest-grade copper mineralisation is present, their effect on permeability seems to be ignored.

- The amount of acid consumed seems to totally ignore the possibility of carbonate minerals and iron oxides affecting the total required. Acid consumption of 10 lb of acid per lb of recovered Cu is very low compared to conventional (non-in-situ) copper leaching operations.

- The economic valuation seems to ignore the cost of drilling the overburden.

- The reference by Excelsior to Taseko’s nearby Florence ISR operation, where a pilot programme proved to be successful, is misleading. The Florence deposit is a copper porphyry that was uplifted to surface and subjected to weathering and oxidation processes before being covered by younger lithologies. The hydraulic conditions have been proven suitable by extensive historical testwork.

Not wanting to be a complete killjoy, there is also an opportunity for Excelsior.

Whereas channelling is a major risk to recover copper from the total skarn package, it creates an opportunity to focus drilling and extraction of the copper along high permeability structures. The geological information points to these structures having the highest grade and (probably) highest CuAS/TCu ratios. The implication is that the kinetics and speed of fluid flow will be such that copper recovery will be fast, requiring less infrastructure and plant.

It would require detailed definition of such targets and accurately intersecting these by drilling of injection and extraction wells. A consequence of this approach is that the channels are a small fraction of the overall volume of the mineralised rock mass, and high-grading would affect the rest of the resource.

Developments since go-ahead decision

After start of construction in December 2018 it took a full year to complete the Stage 1 project which comprised 41 injection and recovery wells and 16 compliance and monitoring wells all to depths of approx. 400m depth. Total project capital expenditure at this stage was US$76M (remember the US$47M per feasibility study?).

Injection of mining fluids started on 31 December 2019 covering an area of 120m x 120 m x 210m (depth) in a closed loop system until the copper in solution reached the required threshold for treatment in the SX-EW plant. Whereas the company claimed that in January 2020 performance levels exceeded feasibility study levels, this was clearly not the full story as in February 2020 it announced it had

“initiated several optimizimation changes to the production wellfield”. The measures were to “assist in acid breakthrough and continued copper mobilization. Breakthrough will be achieved when free acid is detected at designated recovery wells; thereby maintaining the desired pH level (acidity level) where copper will remain in solution”.

Specifically, the wells were made amenable to reverse the fluid flow. In other words, a particular well would be able to first inject and then extract the fluid. The company also announced:

“In parallel, infrastructure is being installed that will allow for concentrated acid to be injected into each well, which will dissolve any reprecipitated copper (copper sulphate) in the area of the pumps, thereby ensuring effective fluid flow. Preventative maintenance programs to limit pump and wellfield down-time are also being implemented”.

The above problems point to:

- The injected fluid not being able to reach the extraction wells.

- Acid being consumed, with the resulting drop in pH resulting in dissolved copper again precipitating.

- Problems with keeping the wells operating properly.

In April 2020 the company used the COVID-19 pandemic as a useful excuse to place the project on care-and-maintenance, to restart an a “small scale” in August. By 30 September 2020 the company had spent another US$6.7M on the project.

With injecting concentrated sulphuric acid solution the problem of precipitated copper was solved (no mention of what the effect was on acid consumption) and the extraction of copper could begin in December leading to the first cathode production. In parallel “expansion of activities to surrounding wells is occurring, with a view to ramping-up to full, nameplate, capacity through 2021”.

Conclusion

The company has had to overhaul the way in which it leaches copper making the feasibility study less of a final and definitive document than the Company would have hoped. Inputs and expectations of production, resource base, and costs are up in the air. It seems that the concerns expressed previously may well be applicable which would have a detrimental effect on contained metal in reserves, metallurgical recovery, acid consumption, operating cost and sustaining capital expenditure.

The fact that copper has been produced is encouraging but more of a marketing ploy than an indication of technical success. It will be important for the company to demonstrate sustainable commercial production at acceptable costs. The Gunnison project again proves the risks of being a pioneer in adopting new technologies. When the go-ahead for any new project, let alone one that incorporates a new technology, is given without substantial empirical evidence and pilot plant work, investors should realise they taken on extremely high risk. Caveat Emptor.

If you are a Family Office investor, or an Institutional investor, and you would like the full report behind this article, please contact matthew@cruxinvestor.com

This week, we have chosen to focus on Excelsior Mining, an example of how old technologies with new applications can be troublesome, how the devil is in the detail, and how not doing enough preparatory work creates major problems for mining companies.

Overview

Excelsior Mining ("Excelsior) (OTCQX:EXMGF) (TSX:MIN) (FSE: 3X3) has a market capitalisation of ~C$260 million, it has just started production from its in-situ leach Gunnison copper project, and is marketing itself with the catchy slogan “We make copper green”.

Not only that, but the share price has almost doubled in recent months on the back of the promise that production would start in 2020, and the Gunnison is in the pro-mining, copper-rich, low-risk state of Arizona. So much to like!

Interestingly the “Excelsior Mining Produces First Copper Cathode” news on 21 December was just a very brief statement, making it seem as if the Company had technically kept its promise, but it did not have a lot of detail to shout about. When we, the good folk at Crux Investor, see something like that, it makes us curious. Is there more to the story? What is really going on?

What follows is a seriously technical analysis of the project, and how the Company has addressed the implementation of the pioneering extraction method on this particular geology. Not wanting to beat around the bush, we can tell you that the company has had to make so many major adaptations that the key de-risking document, the feasibility study, is now largely irrelevant. All inputs and expectations are up in the air.

Indeed there are many risks and pitfalls for the Company that we explain below. All of these factors are likely to have a major effect on contained metal in reserves, metallurgical recovery, acid consumption, operating cost and sustaining capital expenditure. While we love the idea of producing low-carbon, green copper in Arizona, sadly it is largely irrelevant unless the company can prove sustainable and commercial production at an economic cost.

The Gunnison project again proves the risks of being a pioneer in adopting new technologies. When the go-ahead for any new project, let alone one that incorporates a new technology, is given without substantial empirical evidence and pilot plant work, investors should realise they taken on extremely high risk. We feel that Excelsior Mining is now, and will remain for the foreseeable future, a long way from sustainable and commercial production.

For those who do not want to read all the detail further below, this report shows that there are a number of conceptual risks with the business model in terms of geology, geohydrological and metallurgical assumptions, which seem to be borne out by the actual early production, requiring the company to substantially move away from the feasibility study plan. The fact that first copper cathode production was achieved is of little relevance until sustained commercial production is achieved. Caveat Emptor (let the buyer beware)…

What the Company reports

Excelsior has been involved with the Gunnison project in Arizona, USA, since 2007. Along the way it has completed a Feasibility Study (2014, updated in 2016), and bought a defunct heap leach operation called Johnson Camp mine (“JCM”) complete with a solvent extraction electrowinning (“SX-EW”) plant with a capacity to produce 25 million pounds (“Mlb”) per annum.

The feasibility study envisaged production of copper by means of in-situ leaching of a large, low-grade copper deposit and included a three-stage production ramp up, the first using the JCM plant. The economics of the project were (according to the feasibility study) amazingly attractive with an NPV7.5 of US$807M for initial investment of less than US$47M. The study envisaged a nine months “construction” period, which essentially would comprise drilling of injection and extraction boreholes and piping to the plant.

The idea of in-situ leaching is very attractive to bankers and investors as it offers the prospect of not having to go through the dirty business of actually mining rock. Capital expenditure is low, earth disturbance is minimal, and everyone is happy and makes money. Right? Well, not always…

What the Analysts see

Leaching of copper minerals using acid is a proven processing method used in heap leach operations globally. Applying the leaching of copper minerals to in-situ leaching, however, is very unusual. And it is unusual because for it to work, an unusual set of preconditions are needed:

- Copper must be present in minerals amenable to acid leaching.

- No other minerals that consume acid should be present in meaningful quantities, otherwise acid consumption (and overall acid cost) will be prohibitive.

- The deposit must be below the water table, otherwise the injected solution will drain down to the water table.

- The copper mineralisation must occur in permeable rocks with manageable fracturing and flow dynamics so that the leaching fluids can access the copper across a sufficient rock mass.

- The deposit would ideally be encased in impermeable rocks to minimise leakage of acid or pregnant solution away from the deposit.

Excelsior management states quite accurately in their corporate presentation that the method is a very established mining method for Uranium, but this is slightly disingenuous. Although acid is the main leaching agent in Kazakhstan, in the USA the use of an alkali leach is preferred due to the presence of significant quantities of acid-consuming minerals such as gypsum and limestone in the host aquifers.

And this is where the geology comes into play. The Excelsior leaching operation is in an area described as a classic skarn type deposit in contact with an intrusion. Skarns form through metamorphic processes as igneous intrusions react with host rock. The intrusions often interact with limestones, where metals and hot fluids mix, new minerals are formed and then everything cools down as a skarn. After formation, later erosion can expose skarns to the surface where weathering and oxidation of sulphide minerals take place.

Remember that fluid flows preferentially along fractures, and through permeable lithologies. Skarns form preferentially when acidic fluids meet with reactive lithologies (such as limestone). At Gunnison primary mineralisation is related to three main factors:

- Proximity to the intrusion

- Fracture intensity

- Lithology (permeability and reactiveness)

Overprinting that all is an oxidation profile which is the most recent event affecting the sulphides.

At Gunnison, the sulphides at the upper levels of North Star have been oxidised by meteoric water, with copper now mostly present in chrysocolla (Cu₂H₂Si₂O₅(OH)₄) as fracture fillings and vein fill. Chrysocolla is soluble in sulphuric acid, although it is not strictly an oxide mineral. For the geologically-minded among you, it’s hydrated copper phyllosilicate. (Ed….Taxi!)

The cross section also shows the vertical depth of the boundaries to Transitional and Sulfide mineralisation where the copper ceases to be leachable. The criterion used for Oxide mineralisation is a soluble copper grade (“CuAs”) constituting more than half the total copper grade (“CuT”).

As noted above, the development of primary copper-sulphide skarn mineralisation is related to the proximity to the intrusion. The skarn mineralisation preferentially developed in carbonate-bearing units, with the combination of this and proximity to the intrusion leading to the Martin (green colour) and Abrigo Formations (red, yellow and violet) being the primary host units.

According to the feasibility study report there is a strong correlation between total Cu-grade and fracture intensity varying from 0.23% Cu for low intensity fracturing Intensity 1 (defined as less than 5% of core length with pieces less than 10 cm long) to 0.53% Cu for an Intensity 5 (defined as 80%-100% of the drill core pieces being less than 10 cm long) (see Figure 3). This is intuitive because in a skarn, mineralisation is related to fluid flow, and were there are more fractures, there is more copper.

To really dig into the detail, fracture intensity is controlled by several factors: fracturing related to volume loss during skarn development, and fracturing related to pre- and post-mineral faulting. Figure 4 shows the modelled fracture intensity from borehole logs illustrating the strong association with relatively steep faults and a weaker (and thinner) trend parallel to bedding.

The above relationship is however not evident in the block model for North Star as is shown in Figure 5, which is along the same cross section as in Figure 4 implying that the faults are dominantly post mineralisation.

Table 1 shows the mineral resources at a 0.05% TCu cut-off grade and mineral reserves estimated for North Star.

The reserves are essentially the same as resources, but dropping out mineralisation below the Interstate 10 road.

Original Business Plan

Leaching was envisaged by each “production cell” having a central injection well surrounded by four recovery wells on the corners of the square defined by this pattern and each at 30 m distance of the injection cell.

What is a sweep factor, and why should you care?

According to the feasibility study, the amount of recoverable copper depends on something called a Sweep Factor, specific gravity (defined as % of available copper that is contacted by leach solution) and acid soluble copper grade for that 30 m x 30 m x 8 m block of the resource block model.

The sweep factor represents the calculated recovery based on the fracture intensity assigned to the resource block model with an assumed relationship of 20% for Fracture Intensity 1 to more than 80% for Fracture Intensity 3 (20%-50% of the core pieces below 10 cm long) and above. Or in simpler words, the Sweep Factor is a way for Excelsior Mining to make an in-situ recovery estimate from any given block, based on a combination of grade and fracture intensity.

The forecast metallurgical recovery is based on laboratory tests combined with simulation models, not on empirically established factors through a pilot scheme. Therefore, the claim by Excelsior that the injection solution recovery (“ISR”) metallurgical parameters have been established at a feasibility level of confidence sits awkwardly with six assumptions in the section on mineral processing and the 16 mentions of “estimates” or “estimating” in that section of the technical report.

The business plan assumed a stage increase in production, initially at a rate of less than 1,000 t Cu per month, doubling this for Stage 2 in production year 3 and doubling this again for Stage 3 in production years 5 and 6.

What it means for Investors

Potential investors should note that some large players (Magma Copper, BHP and Phelps Dodge) investigated and then rejected further work on this project. Magma Copper actually got to the point of carrying out test work before choosing not to continue. No details of this historic work are provided by Excelsior.

The business plan is based on modelling with major assumptions on how the injected fluid behaves and on achievable leach recovery and on acid consumption. Of particular concern to us, with respect to assumptions, are:

- The assumed Sweep Factor of 80% for rock with a Fracture Intensity with 20%-50% core pieces of less than 10 cm seems overly optimistic.

- The behaviour of solution movement is unlikely to be uniform and unaffected by differences in permeability. In practice fluid movement will prefer the pathways of least resistance, so-called channelling. The geological model and cross section for Fracture Intensity clearly point to the risk of channelling, both along bedding and especially along steeper fault structures. Channelling would greatly reduce the sweep factor by sterilising large volumes of low Fracture Intensity mineralisation from being exposed to the acid solution.

- Whereas there is mention of clay minerals close to the intrusive/skarn contact, exactly where the highest-grade copper mineralisation is present, their effect on permeability seems to be ignored.

- The amount of acid consumed seems to totally ignore the possibility of carbonate minerals and iron oxides affecting the total required. Acid consumption of 10 lb of acid per lb of recovered Cu is very low compared to conventional (non-in-situ) copper leaching operations.

- The economic valuation seems to ignore the cost of drilling the overburden.

- The reference by Excelsior to Taseko’s nearby Florence ISR operation, where a pilot programme proved to be successful, is misleading. The Florence deposit is a copper porphyry that was uplifted to surface and subjected to weathering and oxidation processes before being covered by younger lithologies. The hydraulic conditions have been proven suitable by extensive historical testwork.

Not wanting to be a complete killjoy, there is also an opportunity for Excelsior.

Whereas channelling is a major risk to recover copper from the total skarn package, it creates an opportunity to focus drilling and extraction of the copper along high permeability structures. The geological information points to these structures having the highest grade and (probably) highest CuAS/TCu ratios. The implication is that the kinetics and speed of fluid flow will be such that copper recovery will be fast, requiring less infrastructure and plant.

It would require detailed definition of such targets and accurately intersecting these by drilling of injection and extraction wells. A consequence of this approach is that the channels are a small fraction of the overall volume of the mineralised rock mass, and high-grading would affect the rest of the resource.

Developments since go-ahead decision

After start of construction in December 2018 it took a full year to complete the Stage 1 project which comprised 41 injection and recovery wells and 16 compliance and monitoring wells all to depths of approx. 400m depth. Total project capital expenditure at this stage was US$76M (remember the US$47M per feasibility study?).

Injection of mining fluids started on 31 December 2019 covering an area of 120m x 120 m x 210m (depth) in a closed loop system until the copper in solution reached the required threshold for treatment in the SX-EW plant. Whereas the company claimed that in January 2020 performance levels exceeded feasibility study levels, this was clearly not the full story as in February 2020 it announced it had

“initiated several optimizimation changes to the production wellfield”. The measures were to “assist in acid breakthrough and continued copper mobilization. Breakthrough will be achieved when free acid is detected at designated recovery wells; thereby maintaining the desired pH level (acidity level) where copper will remain in solution”.

Specifically, the wells were made amenable to reverse the fluid flow. In other words, a particular well would be able to first inject and then extract the fluid. The company also announced:

“In parallel, infrastructure is being installed that will allow for concentrated acid to be injected into each well, which will dissolve any reprecipitated copper (copper sulphate) in the area of the pumps, thereby ensuring effective fluid flow. Preventative maintenance programs to limit pump and wellfield down-time are also being implemented”.

The above problems point to:

- The injected fluid not being able to reach the extraction wells.

- Acid being consumed, with the resulting drop in pH resulting in dissolved copper again precipitating.

- Problems with keeping the wells operating properly.

In April 2020 the company used the COVID-19 pandemic as a useful excuse to place the project on care-and-maintenance, to restart an a “small scale” in August. By 30 September 2020 the company had spent another US$6.7M on the project.

With injecting concentrated sulphuric acid solution the problem of precipitated copper was solved (no mention of what the effect was on acid consumption) and the extraction of copper could begin in December leading to the first cathode production. In parallel “expansion of activities to surrounding wells is occurring, with a view to ramping-up to full, nameplate, capacity through 2021”.

Conclusion

The company has had to overhaul the way in which it leaches copper making the feasibility study less of a final and definitive document than the Company would have hoped. Inputs and expectations of production, resource base, and costs are up in the air. It seems that the concerns expressed previously may well be applicable which would have a detrimental effect on contained metal in reserves, metallurgical recovery, acid consumption, operating cost and sustaining capital expenditure.

The fact that copper has been produced is encouraging but more of a marketing ploy than an indication of technical success. It will be important for the company to demonstrate sustainable commercial production at acceptable costs. The Gunnison project again proves the risks of being a pioneer in adopting new technologies. When the go-ahead for any new project, let alone one that incorporates a new technology, is given without substantial empirical evidence and pilot plant work, investors should realise they taken on extremely high risk. Caveat Emptor.

If you are a Family Office investor, or an Institutional investor, and you would like the full report behind this article, please contact matthew@cruxinvestor.com

To read the FULL report, for FREE, please subscribe below.

- Notification By Email When Our Latest Notes Are Published With Immediate Access As Soon As They Go "Live"

- Suggest Future Companies To Be Analysed (Launching Soon)

- Additional Related Notes and "How To's" To Aid You On Your Investment Journey.

Already a subscriber? Sign in